Boeing Has Declared 2025 Its ‘Turnaround Year.’ Should You Bet on BA Stock Here?

/Boeing%20Co_%20corporate%20building-by%20Tada%20Images%20via%20Shutterstock.jpg)

Boeing (BA) delivered its strongest quarterly performance in years, slashing losses while increasing aircraft deliveries as CEO Kelly Ortberg's turnaround efforts are showing tangible results. Boeing delivered 150 airplanes in the second quarter, the most since 2018, while cutting quarterly losses to $176 million from $1.09 billion a year earlier. Revenue surged 35% to $22.75 billion, beating analyst expectations.

The commercial airplane unit posted 81% revenue growth to $10.87 billion, with operating margins improving significantly. Boeing has stabilized 737 Max production at 38 aircraft monthly, the FAA's current limit, and plans to seek approval for higher rates in the third quarter. Cash burn improved to just $200 million from $4.3 billion in the prior year period, with Ortberg targeting positive cash flow generation by the fourth quarter.

Notably, Boeing faces substantial headwinds. The certification of the 737 Max 7 and Max 10 variants has been pushed to 2026, disappointing airlines awaiting these aircraft. The defense division continues to struggle with cost overruns, while a potential strike by factory workers looms after employees rejected a labor deal. Boeing also absorbed a $445 million Justice Department settlement charge related to the fatal 737 Max crashes, underscoring ongoing legal and regulatory scrutiny.

Boeing's operational improvements under Ortberg are encouraging after years of crisis management. However, execution risks remain, including regulatory hurdles, labor disputes, and the need to sustain production improvements.

Can Boeing Stock Recover In 2025?

Valued at a market cap of $167 billion, BA stock is down 50% from all-time highs. However, the shares have gained 25% so far in 2025, significantly outperforming the broader equities market over this time frame.

The company’s latest earnings call revealed detailed production strategies and long-term recovery frameworks that extend well beyond immediate turnaround efforts. The airline manufacturer aims to provide investors with clearer visibility into the path toward sustained profitability.

Ortberg outlined an aggressive but disciplined production ramp plan for the 737 Max program. Following stabilization at the current 38 aircraft monthly rate, Boeing expects to move to 42 monthly units, then progress in five-aircraft increments at no less than six-month intervals. It targets reaching 47 monthly units by year-end, with ultimate production potentially exceeding 60 aircraft monthly using a fourth production line in Everett dedicated to the complex Dash 10 variant.

This methodical approach addresses historical production instability issues while leveraging substantial buffer inventory built during the recovery period. Quality metrics have improved dramatically, with defects down approximately 30% on the Max line and significantly enhanced fuselage quality from Spirit AeroSystems.

Inside Boeing's Turnaround

Boeing Defense and Space achieved its first quarter without charges in years, reflecting improved program management and risk mitigation strategies. The recent F-47 fighter program win represents the largest defense investment in company history and positions Boeing's St. Louis operations for decades of sixth-generation fighter production.

Management emphasized transitioning from problematic fixed-price development contracts to cost-plus arrangements for new programs while actively restructuring existing troubled contracts through customer collaboration, exemplified by the T-7A program modifications.

Boeing’s global footprint provides it with significant advantages amid evolving trade policies. With 80% of commercial supply chain spending directed to U.S. suppliers and 80% of deliveries serving international customers, Boeing benefits from bilateral trade agreements while managing limited input tariff exposure of less than $500 million.

Recent agreements with the EU and UK supporting zero-tariff frameworks benefit Boeing's position as a leading U.S. exporter, with management expressing optimism about continued favorable trade developments.

Is BA Stock Undervalued Right Now?

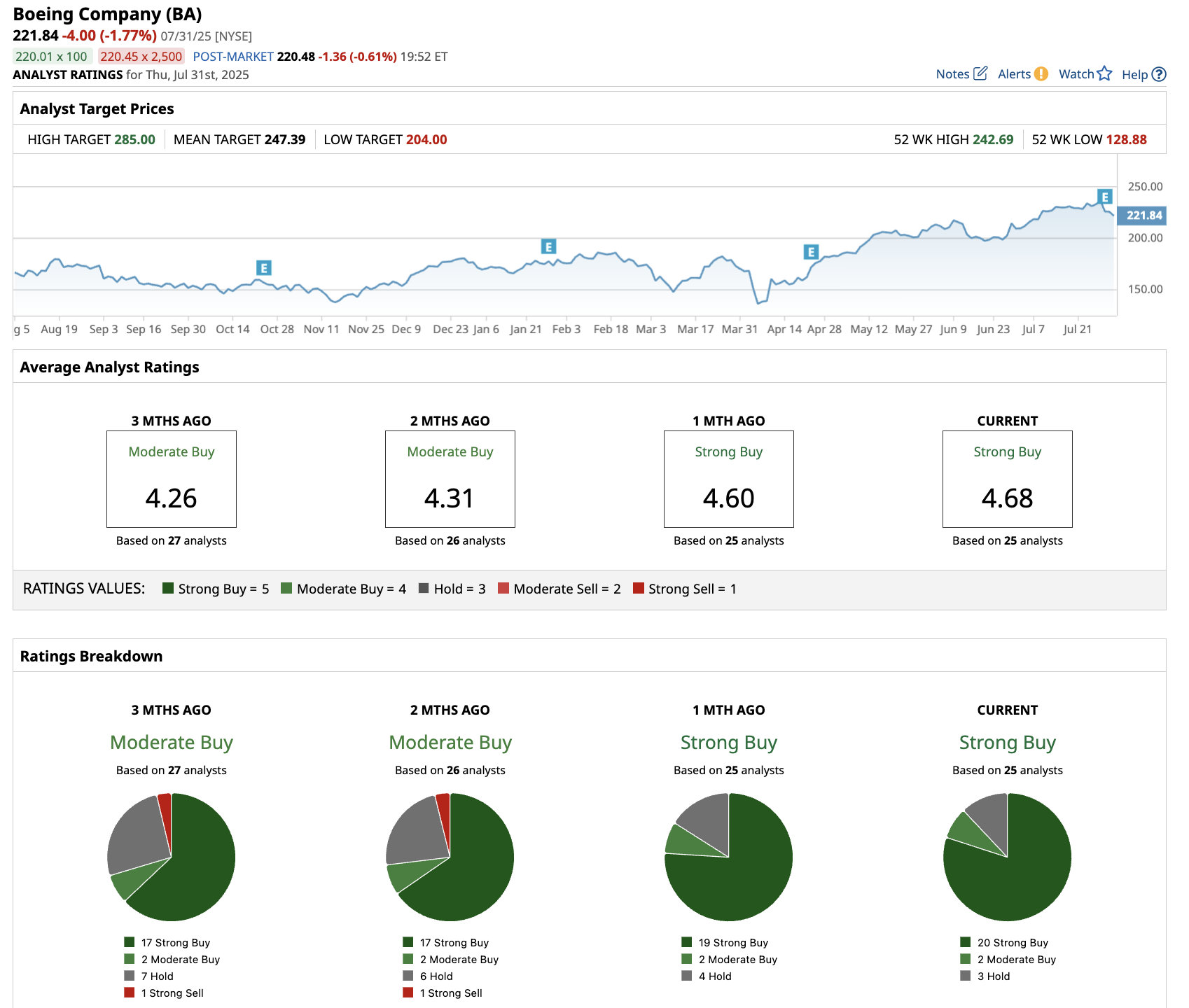

Of the 25 analysts covering BA stock, 20 recommend “Strong Buy,” two recommend “Moderate Buy,” and three recommend “Hold.” The average target price for Boeing stock is $249.21, about 12.3% above Friday's closing price.

Analysts estimate Boeing to report an adjusted earnings per share of $11.92 in 2029, compared to an expected loss per share of $1.95 in 2025. Moreover, its free cash flow is forecast to improve to $12.84 billion in 2029, compared to an outflow of $14.3 billion in 2024. If BA stock is priced at 20x forward free cash flow (FCF), that suggests a market cap valuation of $260 billion in early 2029, indicating an upside potential of 56% from current levels.

On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.